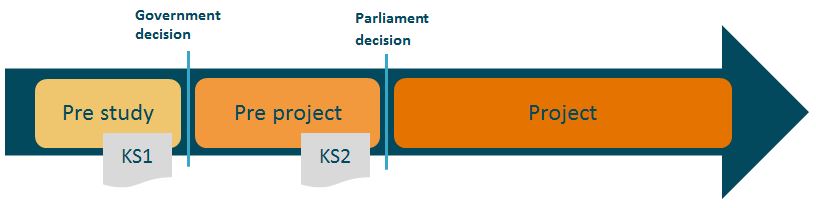

Large public sector investment projects in Norway have to go through an established methodology for quality assurance. There must be an external quality assurance process both of the selected concept (KS1) and the projects profitability and cost (KS2).

KS1 and KS2

Concept quality control (KS1) shall ensure the realization of socio-economic advantages (the revenue side of a public project) by ensuring that the most appropriate concept for the project is selected. Quality assurance of cost and management support (KS2) shall ensure that the project can be completed in a satisfactory manner and with predictable costs.

I have worked with KS2 analysis, focusing on the uncertainty analysis. The analysis must be done in a quantitative manner and be probability based. There is special focus on probability level P50, the project’s expected value or the grant to the Project and P85, the Parliament grant. The civil service entity doing the project is granted the expected value (P50) and must go to a superior level (usually the ministerial level) to use the uncertainty reserve (the difference between the cost level P85 and).

Lessons learnt from risk management in large public projects

Many lessons may be learned from this quality assurance methodology by private companies. Not least is the thorough and methodical way the analysis is done, the way uncertainty is analysed and how the uncertainty reserve is managed.

The analogy to the decision-making levels in the private sector is that the CEO shall manage the project on P50, while he must go to the company’s board to use the uncertainty reserve (P85-P50).

In the uncertainty analyses in KS2 a distinction is made between estimate uncertainty and event uncertainty. This is a useful distinction, as the two types of risks are by nature different.

Estimate uncertainty

Uncertainty in the assumptions behind the calculation of a project’s cost and revenue, such as

- Prices and volumes of products and inputs

- Market mix

- Strategic positioning

- Construction cost

These uncertainties can be modelled in great detail ((But remember – you need to see the forest for the trees!)) and are direct estimates of the project’s or company’s costs and revenues.

Event Uncertainties

These events are not expected to occur and therefore should not be included in the calculation of direct cost or revenue. The variables will initially have an expected value of 0, but events may have serious consequences if they do occur. Events can be modeled by estimating the probability of the event occurring and the consequence if they do. Examples of event uncertainties are

- Political risks in emerging markets

- Paradigm Shifts in consumer habits

- Innovations

- Changes in competitor behavior

- Changes in laws and regulations

- Changes in tax regimes

Why distinguish between estimates and events?

The reason why there are advantages to separating estimates and events in risk modeling is that they are by nature different. An estimate of an expense or income is something we know will be part of a project’s results, with an expected value that is NOT equal to 0. It can be modeled as a probability curve with an expected outcome and a high and low value.

An event, on the other hand, can occur or not, and has an expected value of 0. If the event is expected to occur, the impact of the event should be modeled as an expense or income. Whether the event occurs or not has a probability, and there will be an impact if the event occurs (0 if it doesn’t occur).

Such an event can be modeled as a discrete distribution (0, it does not occur, 1if it occurs) and there is only an impact on the result of the project or business IF it occurs. The consequence may be deterministic – we know what it means if it happens – or it could be a distribution with a high, low and expected value.

An example

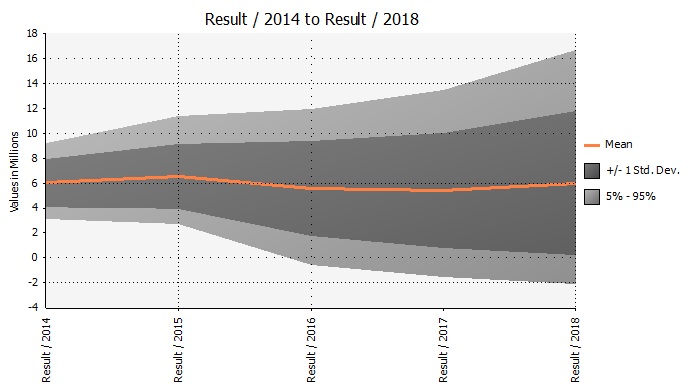

I have created an example using a private manufacturing company. They have an expected P&L which looks like this:

| Example data | 2014 | 2015 | 2016 | 2017 | 2018 | |

|---|---|---|---|---|---|---|

| Sales, # units | 3 500 | 3 600 | 3 750 | 3 900 | 4 050 | |

| Export share | 71 % | 72 % | 72 % | 72 % | 72 % | |

| Value of production | mNOK | 25,3 | 26,4 | 27,9 | 29,4 | 31,0 |

| Variable cost | mNOK | -10,7 | -11,2 | -12,0 | -12,8 | -13,6 |

| Fixed cost | mNOK | -8,8 | -9,1 | -10,6 | -11,0 | -12,0 |

| Result | mNOK | 5,8 | 6,1 | 5,3 | 5,6 | 5,4 |

The company has a high export share to the EU and Norwegian cost (both variable and fixed). Net margin is expected to fall to a level of 17% in 2018. The situation looks somewhat better when the simulated – there is more upside than downside in the market.

But potential events that may affect the result are not yet modeled, and what impact can they have? Let’s look at two examples of potential events:

- The introduction of a duty of 25% on the company’s products in the EU. The company will not be able to lift the cost onto the customers, and therefore this will be a cost for the company.

- There are only two suppliers of the raw materials the company uses to produce its products and the demand for it is high. This means that the company has a risk of not getting enough raw materials (25% less) in order to produce as much as the market demands.

| Event | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| Duty in the EU | 25 % | 25 % | 25 % | 25 % | 25 % |

| Probability | 0 % | 10 % | 20 % | 20 % | 30 % |

| Impact mNOK | -5,1 | -5,4 | -5,6 | -5,9 | -6,3 |

| Lack of raw material | 25 % | 25 % | 25 % | 25 % | 25 % |

| Probability | 0 % | 0 % | 20 % | 25 % | 30 % |

| Impact mNOK | -3,7 | -3,9 | -4,0 | -4,1 | -4,4 |

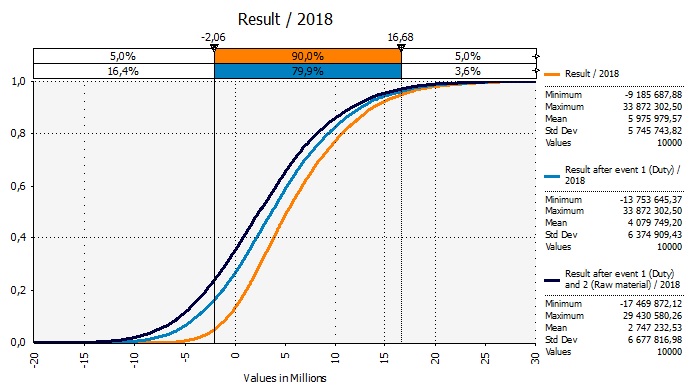

As the table shows the risk that the events occur increase with time. Looking at the consequences of the probability weighted events in 2018, the impact on the expected result is:

The consequence of these events is a larger downside risk (lower expected result) and higher variability (larger standard deviation). The probability of a 0 result is

- 14% in the base scenario

- 27% with the event «Duty in the EU»

- 36% with the event «Raw material Shortage» in addition

The events have no upside, so this is a pure increase in company risk. A 36% probability of a result of 0 or lower may be dramatic. The knowledge of what potential events may mean to the company’s profitability will contribute to the company’s ability to take appropriate measures in time, for instance

- Be less dependent on EU customers

- Securing a long-term raw materials contract

and so on.

Normally, this kind of analysis is done as a scenario. But a scenario analysis will not provide the answer to how likely the event is nor to what the likely consequence is. Neither will it be able to give the answer to the question: How likely it is that the business will make a loss?

One of the main reasons for risk analysis is that it increases the ability to take action in time. Good risk management is all about being one step ahead – all the time. As a rule, the consequences of events that no one has thought of (and thus no plan B is in place) are greater than that of events which have been thought through. It is far better to have calculated the consequences, reflected on the probabilities and if possible put in place risk mitigation.

Knowing the likelihood that something can go horribly wrong is also an important tool in order to properly prioritize and put mitigation measures in at the right place.